CAPITALISE ON MARKET VOLATILITY WHILE TRADING WITH STP BROKER

CAPITALISE ON MARKET VOLATILITY WHILE TRADING WITH STP BROKER

FxGrow clients have once again safely navigated turbulent markets thanks to the specific benefits and characteristics of their trading accounts. In fact, all FxGrow trading accounts enjoy negative balance protection, tight spreads, no limits on orders, and of course the ever resilient STP model.

Straight through processing of orders inherently provides a number of safeguards for traders who are not exposed to the risk of re-quotes or rejection of their orders. This stems from the incredible speeds at which trades are executed, in less than a nanosecond in fact. In other words, the prices you see are the prices you get, because there are simply no delays in the orders being processed. FxGrow has been an STP broker since it was launched, meaning that every single FxGrow trading account, is an STP account.

The importance of trading with the right brokerage is critical for trader protection. Just this week the markets were rocked by the sudden and dramatic drop in the Dow Jones index. The Nasdaq and S&P 500 also took a beating following underwhelming earnings reports from corporate giants Chevron, Exxon, and Apple, also amid fears that interest rates could be raised due to growth in US wages. The losses were significant and costly, prompting traders around the world to scramble as the ripple effect moved across Europe and in to Asian markets too.

Extreme volatility and sudden market movements are always a test for brokers. Over the years, many cases have been witnessed and documented where the negative consequences were passed on to traders, and in some cases brokers have even gone out of business.

Meanwhile FxGrow continues to stand strong, providing total protection for its clients and their funds, who are able to rest easy knowing that they are shielded from any devastating impact. Indeed, many FxGrow traders have been able to capitalise on market volatility to realise substantial gains. This is due to the fact that FxGrow, regardless of market fluctuations:

ü Does not increase margin requirements

ü Does not add any extra limits on orders

ü Provides Negative Balance Protection

ü Offer the best market prices with the lowest spreads available

All the above factors allow our traders to recover and benefit from the opportunities that abound during market volatility.

Once again, we have seen that FxGrow holds the formula to success and longevity in the trading markets space, offering a level of stability that is becoming increasingly important.

Last but not least, FxGrow caters to investors of all experience levels and investment size, offering several account types that can be opened online securely, within just a matter of minutes. Free practice accounts are also available so go ahead and register with us and start trading with a true STP broker!

DXY: Hammered Again By Trump, FOMC is Next??

The Us Index extended the down consolidation sessions, still trading below 90 level throughout the week and has failed to give any new clues about next destination. On Wednesday Asian trading session, the DXY traded narrow with $0.25 range, although expectations were for more as Trump was giving the State of Union Speech.

The president, instead of an optimistic content as expectations were placed by analysts, Trump delivered a speech that projected sadness reminding the audience of how unfair trade treaties are abusing the U.S and a more robust push-back against unfair trade practices by other nations. It is obvious by now how Trump favors a lower US Dollar where it serves his purpose regarding imports - exports and building a strong economy as the president pictures.

The next main event for today will be US Feds rate decision the along FOMC statement.

The first section regarding rates, odds are placed at more than 95% for a no change at current 1.50% with inflation on 12 months’ basis continues to run below FOMC's target at 2%. As for employment sector, a strong data has been demonstrated and has hardly fell below 4.1% which indicates a healthy sector. Average Earnings and Core Durable Goods Order are ticking up positively.

Stating the above leaves the statement and its content as the vague second section where the Yellen & Co. could play the market as they present their hidden cards. The main focus will be on what's hidden for 2018, more hikes or less hikes. Odds for March rates are expected for an increase at 93% as Goldman Sachs stated. As for the Fed's balance sheet, it is likely to bring anything new.

A hawkish scenario would state that recent data is showing a strong economy and despite inflation missing target, we expect that numbers will add up and target will be met, thus there will more rates hikes in 2018 as the Feds grow intolerant for inflation.

A dovish scenario would hint that inflation is still running below 2% target, and until we see a progress or data ticking up, the U.S Feds has no reason to rush. This leaves market to run depending on next CPI report. Also, March hike is not a done deal yet, we may have to take another look at coming data, hence decreasing the odds.

The most common scenario would be a neutral tone where nothing new will be laid on out on coming rates, nor balance sheet reduction since its Yellen last event where she heads the FOMC, and Powell will take over as next nominee, but still Yellen could surprise us.

Finally, market has to pay attention for this part. What if market was already trading the buck based on expectations for a hike and the sharp depreciation for DXY was the result on this scenario? We could see a reversal the US Index with a remarkable rally and sharp tone, pushing all rival currencies down. The suggested scenario has happened before when Trump took the oval office. A hike was delivered and the DXY plunged severely as buy the rumor, sell the fact.

Hours from now and all the image will be clear.

US Index Technical overview:

Crude Oil Hits Three Years High Over Disappointing EIA Report, Awaiting U.S Inventories

Crude oil marches confident this week adding $2.15 pb, and clocked three years high at $63.56 on Wednesday pushed by disappointing EIA report showing a sharp decline in U.S Inventories and successful OPEC efforts keeping WTI at high levels.

EIA report showed a severe drop in U.S Inventories on Jan 5th 2018 by 11.2M barrels reaching 416.6M barrels while expectations were at 3.9M barrels. For now, EIA recorded a drop for the eight consecutive weeks.

On the other hand, The Organization of the Petroleum Exporting Countries (OPEC) and its allies, including Russia are maintaining supply limits in place in 2018, a second year of restraint, to minimize a price-denting glut of oil held in inventories. (Reuters).

Markets are awaiting U.S Inventories data release today at 3:30 PM GMT, in case of confirmation, the draw will be the largest since Sept. 2, 2016. U.S. stockpiles fell by 14.5 million barrels during that week.

“We expect oil demand growth to outpace non-OPEC supply growth in both 2018 and 2019,” Standard Chartered analysts said in a note. (Reuters)

“In our view, the back of the Brent and WTI curves are both still underpriced. We do not think that prices below $65 per barrel are sustainable into the medium term.”

The increase in prices is expected to rise gains in U.S. production during 2018, offsetting curbs by others.

Crude oil technical overview ahead of U.S Inventories:

FOMC Overview And It's Impact ON CFD's

Today, the U.S Federal Reserve will announce the rates with high expectations for a no change and will maintain at current 1.25%. Along with it, FOMC economic projections, a statement, and finally a press conference which will create chaos in the market depending on the content of the answers. In case Yellen has the intention and was serious by gearing up the market, then expect intended hints because Yellen usually delivers vague speeches, leaving market confused. FOMC will focus on two elements, December odds rates and more importantly, current QE program and the edition that will undergo.

First regarding rates, it is highly expected that Yellen & Co will leave rates at current 1.25% especially that last PPI was projected at 0.3% and the Producer Price Index slipped by 0.1% and recorded 0.2%, while consesus aimed at 0.3% . On the other hand, Inflation last recorded in August was 1.9%, still below 2% as a central bank aims. Come to Core Retail Sales last week, a disappointing data with -0.2%, falling from 0.4% last shown, while expectations were at 0.5%. Last but not least, PCE, Fed's preferred measure added no change at 0.1%. Adding all these elements, increasing rates will be postponed for another session, and as Yellen previously expressed, any increase for current rates will depend on how market is performing and recorded data

Enough said, market already knows the above and there is no doubt about it. The real question will be, is end of 2017's rates December is still on the table? In case yes, what are the odds for that (currently below 50%). Any hints that rates odds has increased, and the Feds are serious expressing concerns that inflation has increased by 0.3% since last recorded 0.1%, and its meeting their projections, and its being intolerant, this to be taken hawkish and will boost the buck. On the other hand, a dovish scenario will be that inflation is still below 2%, and any rate decision will be subject to further coming data.

Second, Now this part has been covered, we come to the balance sheet that Yellen promised in last FOMC meeting relatively soon. Market is expecting date and numbers, any failure to deliver on this part, the DXY will take a dip. In case an announcement came out that starting by October and December trimming the balance sheet by $10 billion a month for the first three months, $20 billion per month for the next three, and on and on until it hits a pace of $50 billion per month. This will create a high demand of the U.S Dollar and Index will peek (Hawkish Scenario). In case dates were set without numbers given, this will be left for the market and how they feel about it as its considered neutral. Just a reminder that during last Jackson hole meeting, Yellen has announced that the QE ( Quantitative Easing Program or Bond Purchasing ) has been introduced after 2008's crisis and has kept global monetary policy system safe and its still exist for a reason. One can only wonder how far will Yellen go giving up such a measure especially that Trump is in the oval office.

Finally, recent FOMC members who crossed wires during Sep has expressed a hawkish tone towards rates especially on Dec, we will see how far their statement is serious tonight. On the other hand, it is highly expected that Yellen will end its term as head of U.S Federal reserve during 2018 and be replaced by Cohn, Trump's favorite as they both prefer low rates.Trump has already expressed that previously and hinted for Yellen his desire for low U.S dollar which has kept the greenback from seeing the light, if not intentionally, then by his demand for building the wall, elevating the sharp war tone on NK, delay on tax plan, health care bill, last but not least, his twitters, always tackling the Dollar, and so on.

There is a scenario that Yellen, and out of her concern for U.S monetary policy could take market off guard by a rate increase, if not today, maybe during December even if expectations hints for a no. In case of that, market will be caught off guard and U.S Index will be rallying with fire and fury just like BOC did last meeting where they hiked.

After expressing the above fundamentals, here is technical overview for CFD's including currencies, commodities, and indices to have an idea where and will market will head. CFD's Technical Overview https://goo.gl/mQnHHQ

UK Election With Potential Impact On Forex Market

Thursday, June 8th 2017, UK election will take place and market will undergo sharp volatility with a reminder of how Sterling was a on chaotic ride between ups and downs during Brexit, but perhaps this time with less severe volatility, but there will be action in the market bringing opportunities for traders.

The latest general election polls indicates that the gap between Labour and the Conservatives has narrowed further still. As uncertainties are still hoovering without any clear signs on how final result could end. At such moments, gold (as safe haven) will be the greatest winner during UK election and today's sharp rallies are only a starter and it will prolong before and after the election take place depending on the final outcome, along with it GBP. Below are possible scenarios on what market should expect.

1- What Will happen if current PM May wins:

Although recent polls are thin between May and Corbyn especially after UK's terror attacks, the Conservatives are still more likely to win over the Labour and it's in the market's mind as forecast. The battle over number of seats in the Parliament is what will drive the market.

In case Conservatives managed to score more than 125 seats would be seen unexpected with a positive shock wave for the market and Sterling will be on a stand-by motion for 2017's highest record and UK stock market could bearish after collapsing by strong currency.

Markets are already expecting that May representing Conservatives, will collect a number between 70 and 125 seats, in case this scenario happened, expectations for market to stay put without adding anything new to an already anticipated result. In other words, the news is already expired.

Alternative scenario, in case PM May failed to add anything new, the reason for calling snap election is to increase Conservatives seats, market could take it as negative outcome sending selloffs wave and market could abandon GBP on failure of delivery.

Now in case the Conservatives failed to score above 70 seats. This to be considered negative for market and the British Pound could be tanked seeing 1.2500 potential, a ride from where the Sterling took after May called for snap election. Alternatively, UK's stocks will hike and increase in value.

2. What will happen if Corbyn wins:

Before we get to the results, let's take a brief outlook on what Corbyn holds in his agenda. Corbyn economic plan as a reform is considered old-fashioned and his tax plan proposed would send a message for potential investors as to think twice before committing to UK's economy.

There is no need to extend further more, but as a reminder, a negative shock wave will be dwelling in the market's head, along with it collapsing for Sterling which will take some time (long run) to overcome losses. Part of what happened during Brexit and the hard journey that GBP/USD had to bear to reach current level.

Note: During and after coming UK General Election, FxGrow will introduce:

1 -NO CHANGES IN MARGIN REQUIREMENTS

2- NO CHANGES IN MAX. LEVERAGE AVAILABLE.

3- FULL NEGATIVE BALANCE PROTECTION.

" Note: This analysis is intended to provide general information and does not constitute the provision of INVESTMENT ADVICE. Investors should, before acting on this information, consider the appropriateness of this information having regard to their personal objectives, financial situation or needs. We recommend investors obtain investment advice specific to their situation before making any financial investment decision. "

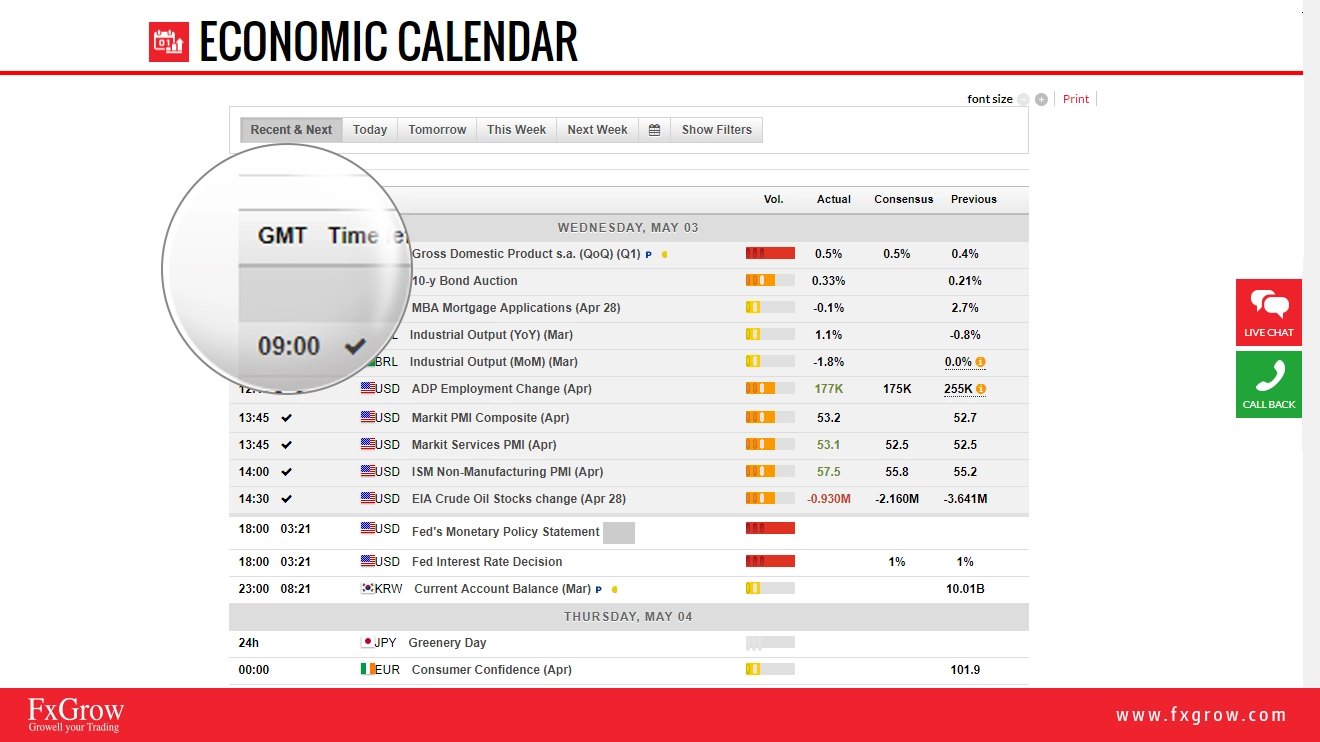

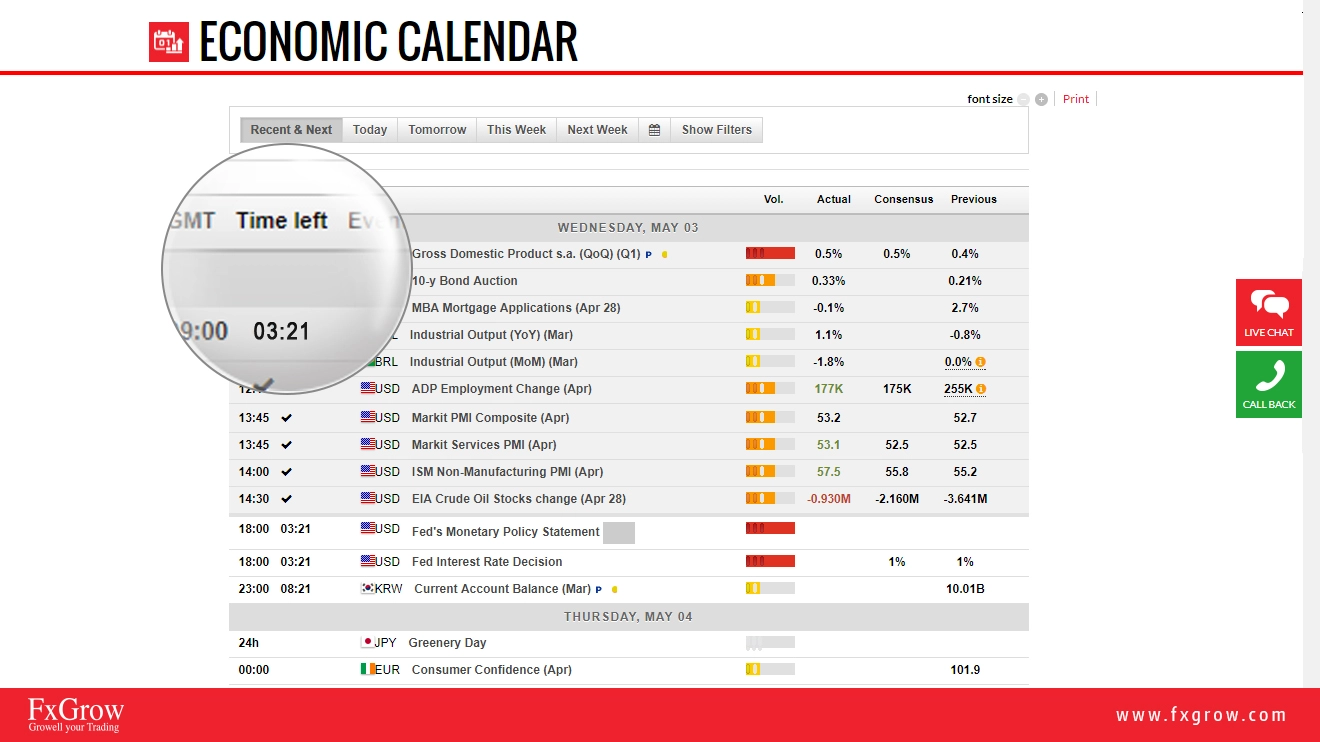

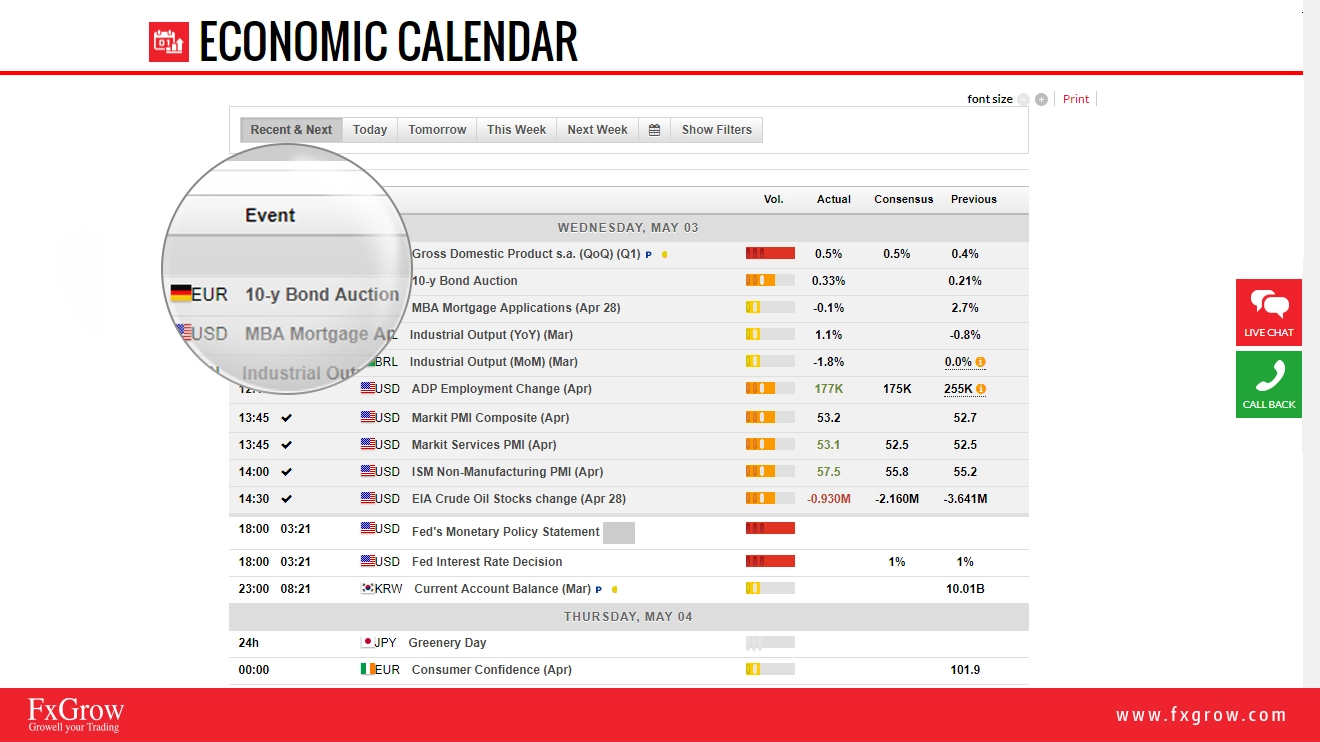

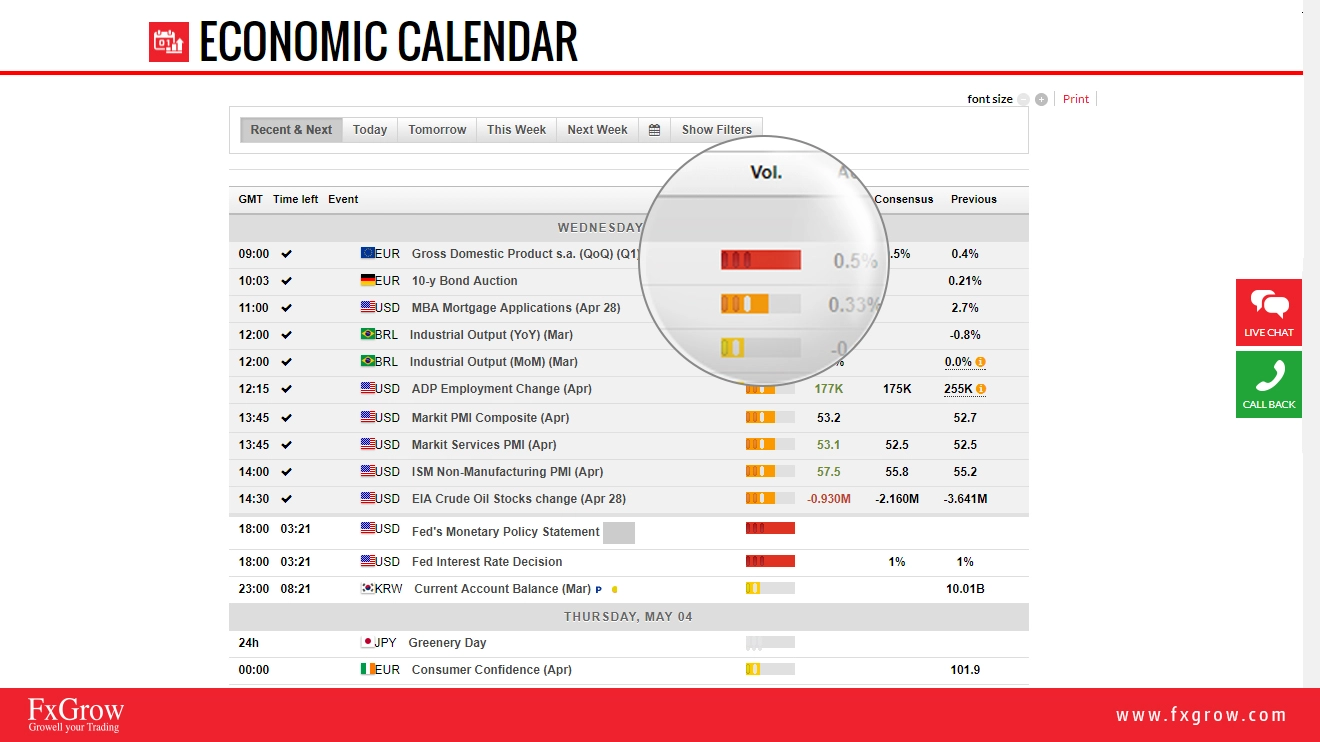

New Economic Calendar

FxGrow is excited to inform you that we have updated our economic calendar with a new interactive version. This version is more interactive and more detailed. Please check below how to read and anticipate data before and after the release from left to right. You have the choice either to choose recent and next economic news, today's full economic news, tomorrow's economic news, weekly economic news, and also next week if you are looking for expanding your research. Also, if you click on filters, you can choose countries that you wish to see their economic release depending on your trading instruments.

Please check below instruments available on economic calendar with visual and a brief elaboration on how to read and anticipate EC.

1- First of all, it's all about timing being prepared before and after the economic news is released. GMT, is a united timing set as Greenwich Mean Time set as United Kingdom timing. You can check your time zone and how many hours it's different from UK, depending on your country Latitudes

2- Time left indicates how many hours, minutes and seconds left to the data release.

3- Event, is the title of the economic data or news that was and about to be released.

4- Vol. indicates the level or impact or degree of importance. A red color indicates a high level of impact of the currency, an orange signifies a medium impact, and yellow indicates the lowest level of importance.

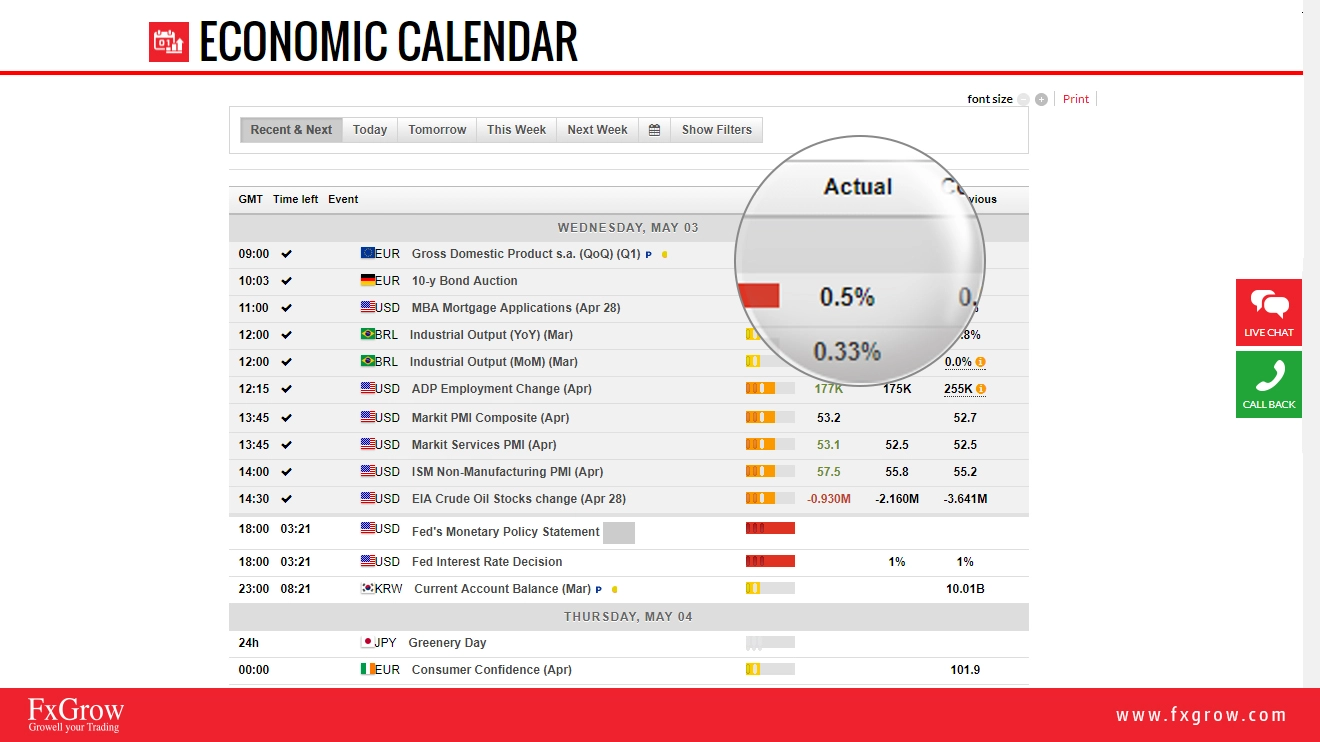

5- Actual: It is the result of the published news that is about to be released for today. It is the real and true data released by the country.

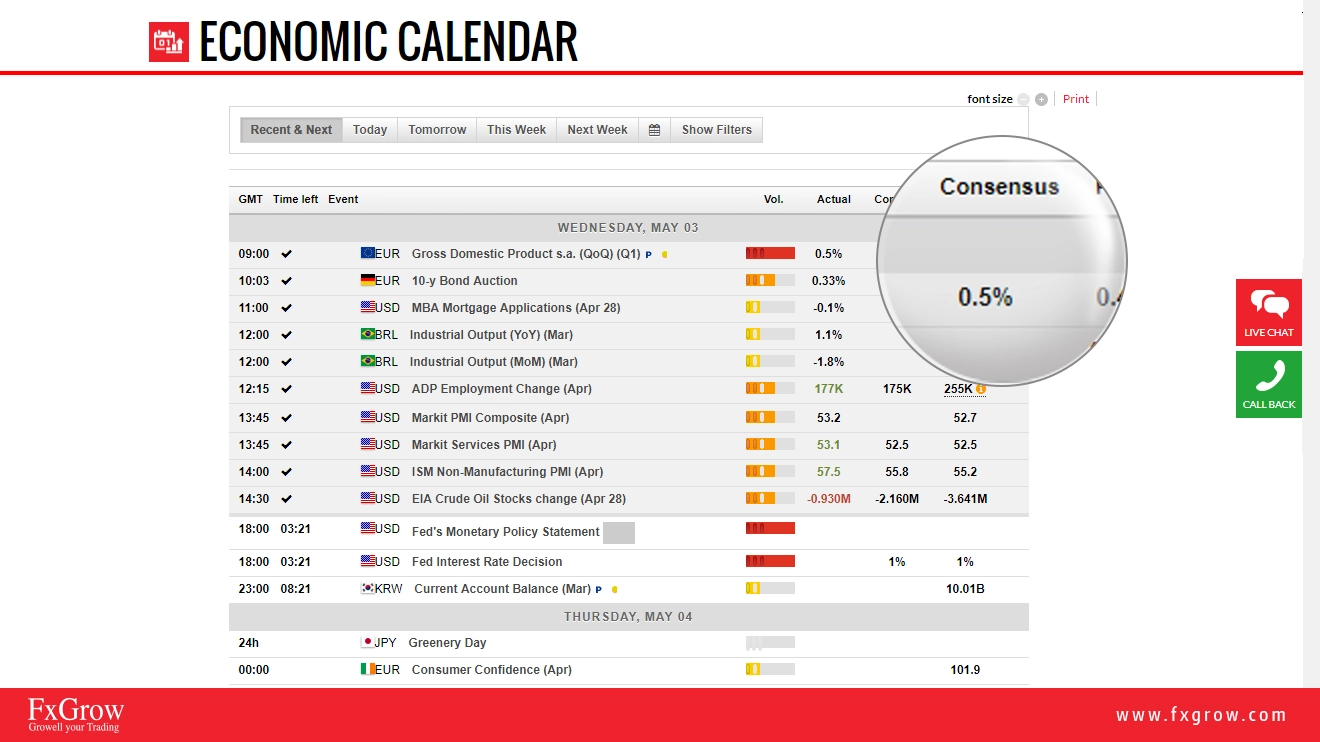

6- Consensus: It means the forecasts for possible outcome of the economic data. As the word forecasts means, the data mentioned is an expectation or possible outcomes, the expected data is not accurate and the data about to be released can either be lower, higher, or the same result.

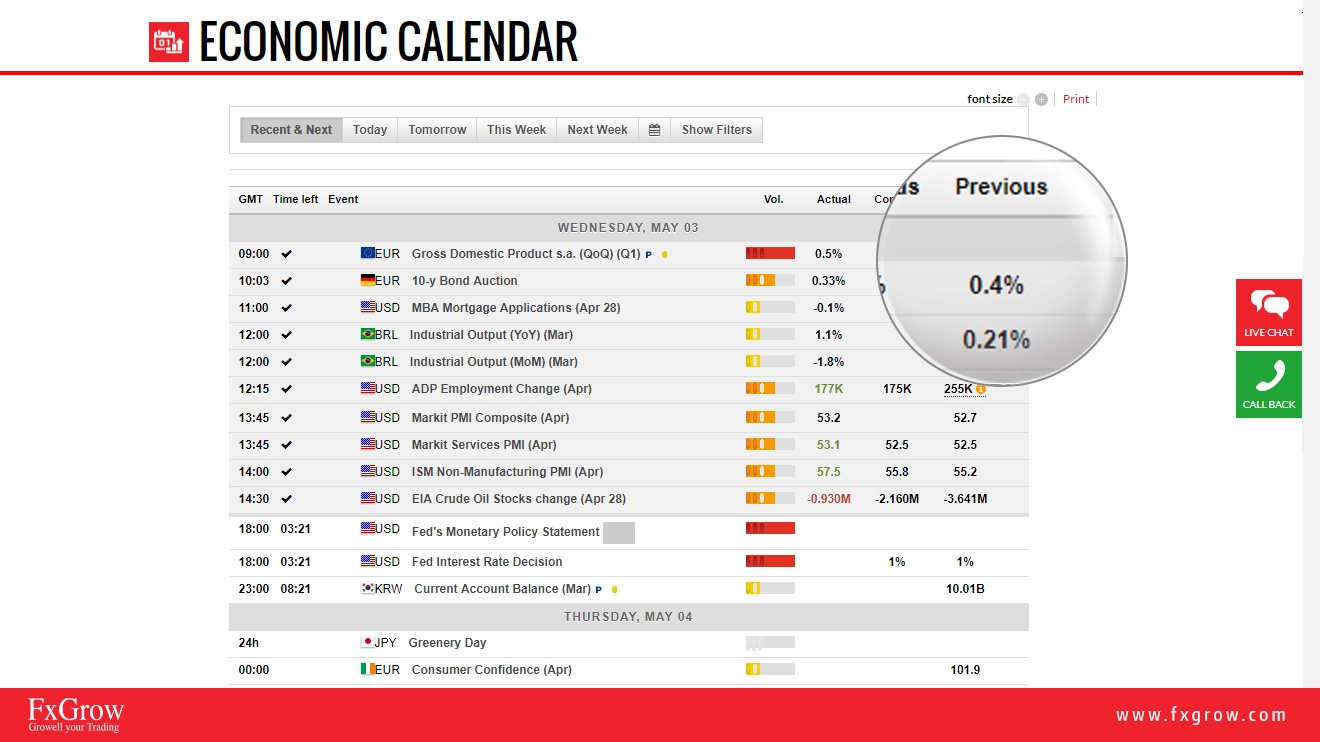

7- Previous: It's an indication of the last economic data released.

8- Also, now you have the option to read deeper analysis about the news itself, just by clicking on the news, a small paragraph will appear with details mentioned with details about its previous impact, volatility, true range, and deviation. This is meant for deeper, wider view for the event.

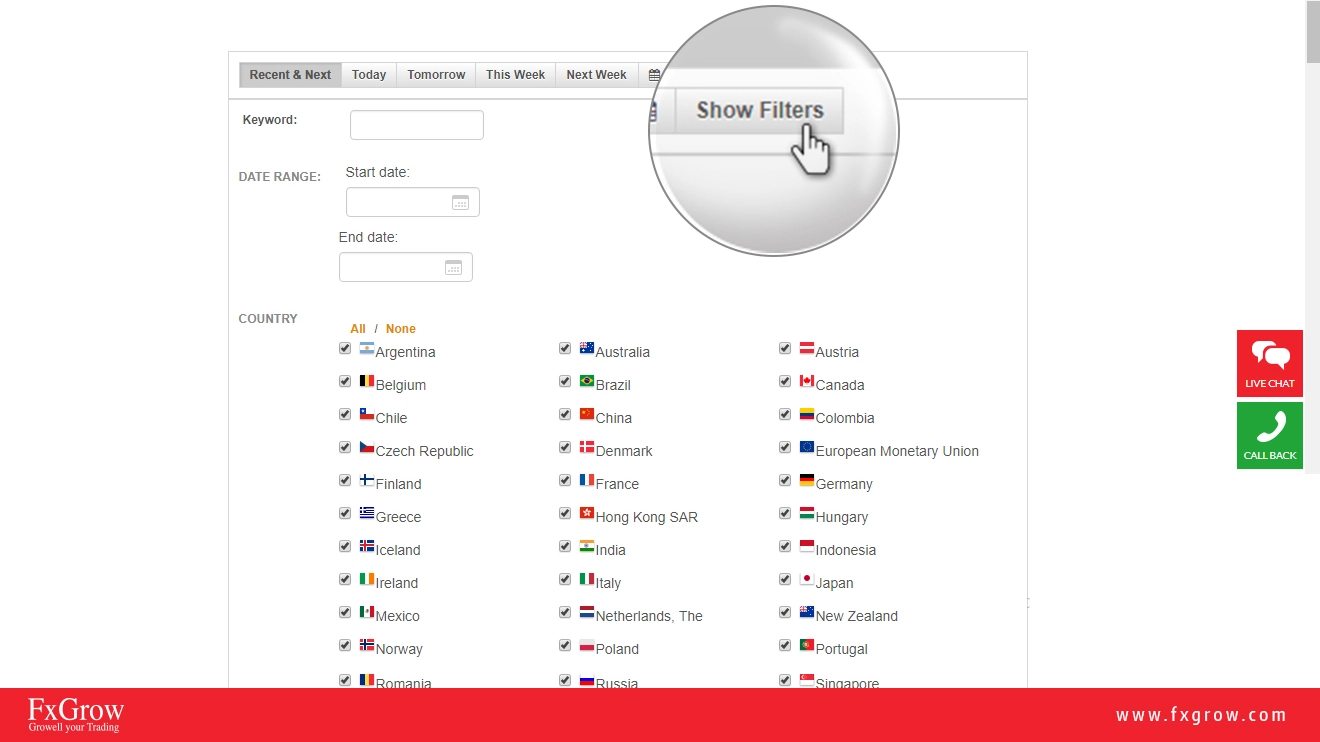

9- Also, part of providing all global economic and financial events, FxGrow added the filter option where you, as a trader, now you can choose the countries that you wish to stay updated with their economic data and latest released news. This is intended to minimize and maximize economic data input.

10 - After you have checked the above details, the final part is how to read and trade upon data released.

A green Color = Good for Currency - Actual or consensus> Forecast

A red color = Bad for Currency – Actual or Consensus < Forecast.

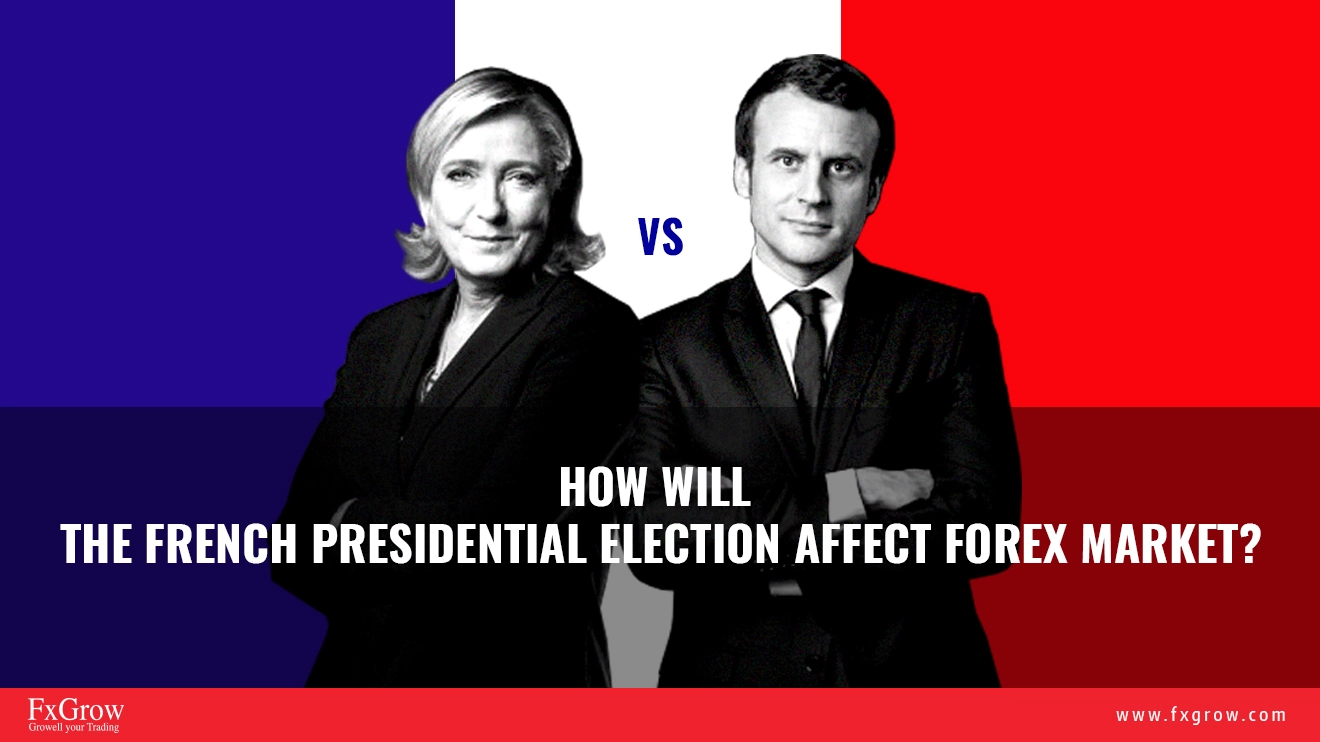

How Will The French Presidential Election Affect Forex Market?

Time is ticking, French Presidential Election is knocking on doors and this Sunday, French citizens will have the upper hand as they will decide the EU coming future. For once and for all, Frexit will either re-surface or lay to rest depending on the final outcome this Sunday, May 7th 2017. Bare in mind, whoever wins, there will be consequences on the financial market in general, but EURO will take center stage.

Two candidates ( Macron and Le Pen ) has qualified for the final round, and latest polls indicates that Macron is ahead by 60% and Le Pen is behind by 40% taking into consideration that Fillon who came third in the first round has requested his supporters to add their voices to Macron, and Melenchon as left-wing voters are committed to prevent Le Pen from claiming the rein. But that's election, and nothing is guaranteed, and if we go back a bit in history to U.S elections, polls gave Clinton the priority, and market saw Trump triumph as shocking. So below, we will place the possible scenario and the outcomes despite what polls are signaling and indicating although their is one major difference, the gap poll between Macron and Le Pen is way wider than the gap poll that was between Clinton and Trump.

Scenario one ( Macron Winning the French Election):

Market is already priced in on the fact Macron is winning, and during the first round, as Macron was heading the polls, EURO gaped upward, hitting five months highs, and if Macron is officially declared a president, optimism will increase further more pushing EURO to higher levels with 1.10 or 1.11 as target. Macron calls for a sharper Pro-EU tone and sees EU as a whole nation, which should push EU stocks and CAC40 even higher. On the other hand, Gold gapped downward and later on fell by $30 as political tension seemed to fade away.

Scenario two ( Le Pen winning the French Election ):

Before we discuss what will happen to the market, first lets briefly state what Le Pen stands for. Le Pen represent the total opposite of Macron and sees France as an independent nation, calling for a referendum by French citizens to vote for a departure from European Cartel following the path of UK voting for Brexit. We all remember what happened on Brexit and how the EURO and British Pound was on a roller coaster. If Le Pen was declared winner, then fear will creep into minds and gossips about Frexit will be on the French menu. Take at that, EURO will start the process of depreciating gradually with 1.600 and 1.500 as target as early signs. The more Frexit approaches and becomes a reality, markets could witness even lower levels than 1.500. European stocks will plunge as well CAC40, and the biggest winner will be gold as geopolitics play its role in pushing the yellow metal into higher levels for 2017, being a sacred haven substitute.

French presidential candidate Marine Le Pen crossed the wires last minutes today, via Reuters, noting that Italy would welcome her efforts to renegotiate the Euro, in case she wins the election.

The below fourth and fifth scenarios are less likely to happen, but part of analysis, it's our duty to include all possible outcomes.

Scenario Three: It's never about who wins

It's never about who wins despite the fact Le Pen or Macron being victorious. The fact the France has a new president will push EURO higher. During U.S elections, market and analysts were divided with different opinions on how will the market perform and will happen to U.S Dollar taking into consideration what Clinton and Trump, each of them stand for. The fact there was a president in the oval office boosted U.S Dollar and American Stocks rallied, add to that, Dow Jones hit news records. Taking at this, we could see a possible scenario on the short run, but as time narrows down with each president agendas (long run), we will see how EURO and EU Stocks will perform depending on impact level of each president agenda.

Scenario Four: Market is already Priced in that Macron is a Winner:

This is the least possible scenario. Market has placed its bets that Macron is a winner, and has traded on this fact. The optimism is expired, EURO and EU Stocks has already peeked as if France is staying in the EU, so it will bring nothing new to traders mind. EUR and EU Stocks will stay put and even make a minor correction upward or downward. Later economic data will shape up the Forex market including EURO, EU Stcoks, and CAC40, depending on the outcome (Economic Data) as part of ebb and flow between currencies.

" Note: This analysis is intended to provide general information and does not constitute the provision of INVESTMENT ADVICE. Investors should, before acting on this information, consider the appropriateness of this information having regard to their personal objectives, financial situation or needs. We recommend investors obtain investment advice specific to their situation before making any financial investment decision. "

Heads Up For FOMC Meeting Tonight

.webp)

Market is poised with confusion about FOMC meeting tonight and possible outcomes. It is largely expected more than 90%, that US Fed are to leave current Interest Rates at current 1.00% without any changes which should send a short-term negative reaction, awaiting FOMC statement.

Now we have established the fact the U.S Central Banks will not touch the rates tonight, the statement and the following press conference will take center stage and as policymakers seem to shirt the path of monetary and fiscal from rates to the balance sheet. Yellen and Co. will cautiously choose their words with efforts to withhold U.S Dollar from further declines.

Last March during FOMC meeting, Yellen mentioned that changes on the balance sheet will depend on economic conditions, and latest data including weak GDP last week and poor macroeconomic readings have lead markets to doubt that the central bank will raise rates two more times this year, with three "live" meetings ahead that could offer such outcome: June, September and December.

If the FOMC meeting hinted that market should not expect a hike during June, markets will assume that chances for additional rate increase this year will be left at one taking into consideration that the U.S Fed will unlikely to raise rates on two consecutive sessions. This would result in a negative impact for U.S Dollar. But in case June is left on the rate menu with high odds, a chances for two hikes including this June and end of Year 2017, this should handle boosting the U.S Dollar for the short-run.

A hawkish scenario is unlikely, and unless the Fed clearly indicates that two rate hikes are still on the table, dollar gains are likely to be short-term and limited, not enough to revert the sour tone that surrounds current pale U.S Dollar. Last U.S Fed hike that resulted in 0.25%, it was seen that U.S Dollar dipping instead of surging. This was justified that March hike was largely expected and market traded on " Buy the rumor, sell the fact".

Heads Up for FOMC meeting Tonight

Market is poised with confusion about FOMC meeting tonight and possible outcomes. It is largely expected more than 90%, that US Fed are to leave current Interest Rates at current 1.00% without any changes which should send a short-term negative reaction, awaiting FOMC statement.

Now we have established the fact the U.S Central Banks will not touch the rates tonight, the statement and the following press conference will take center stage and as policymakers seem to shirt the path of monetary and fiscal from rates to the balance sheet. Yellen and Co. will cautiously choose their words with efforts to withhold U.S Dollar from further declines.

Last March during FOMC meeting, Yellen mentioned that changes on the balance sheet will depend on economic conditions, and latest data including weak GDP last weak and poor Poor macroeconomic readings have lead markets to doubt that the central bank will raise rates two more times this year, with three "live" meetings ahead that could offer such outcome: June, September and December.

If the FOMC meeting hinted that market should not expect a hike during June, markets will assume that chances for additional rate increase this year will be left at one taking into consideration that the U.S Fed will unlikely to raise rates on two consecutive sessions. This would result in a negative impact for U.S Dollar. But in case June is left on the rate menu with high odds, a chances for two hikes including this June and end of Year 2017, this should handle boosting the U.S Dollar.

A hawkish scenario is unlikely, and unless the Fed clearly indicates that two rate hikes are still on the table, dollar gains are likely to be short-term and limited, not enough to revert the sour tone that surrounds current pale U.S Dollar. Last U.S Fed hike that resulted in 0.25%, it was seen that U.S Dollar dipping instead of of surging. This was justified that March hike was largely expected and market traded on " Buy the rumor, sell the fact".

All You Need to Know About French Elections And Its Impact on EUR/USD Levels

French elections are knocking on doors and bets are already placed by markets on every candidate and their agendas. Now, whoever qualifies for the second round, will have a huge impact on market despite the outcome. the race is tight, and on Sunday, 23rd of April, French citizens will elect two candidates out of four who shall be eligible for the next round on May the 7th. Although this may seem irrelevant, but market should pay attention that UK parliament will be dissolved on May the 2nd, and if both dates ( May 2nd & May 7th), combined together, market will be chaotic taking into consideration UK and France, two nations representing top ten markets contributing to global economy.

Note: There are eleven French candidates running on April 23rd, but according to polls, it's more likely that the four candidates; Le Pen, Macron, Mélenchon, and Fillon being triumphed or qualifying for second round on May 7th 2017. In case one of the four nominees managed to secure more than 50% of French voters, then the second round on May 7th will be discarded and a winner will be announced.

First, let's identify the four French candidates and their agenda, after that, the picture will purify and how the market will head especially for the EURO coming future.

1- What does Le Pen want:

- Negotiation with Brussels on a new EU, followed by a referendum.

- "Automatic" expulsion of illegal immigrants and legal immigration cut to 10,000 per year following an immediate total moratorium.

- "Extremist" mosques closed and priority to French nationals in social housing.

- Retirement age fixed at 60 and 35-hour week assured.

2- What does Macron want:

- €50bn (£43bn; $53bn) public investment plan to cover job-training, exit from coal and shift to renewable energy, infrastructure and modernisation.

- Reimbursement of full cost of glasses, dentures and hearing aids.

- Big cut in corporation tax and more leeway for companies to renegotiate 35-hour week.

- Cut in jobless rate to 7% (now 9.7%).

- Ban on mobile phone use in schools for under-15s and a €500 culture pass for 18 year olds.

3- What does Mélenchon want:

- Voting from age of 16 and a "Sixth Republic" to replace the existing presidential system.

- Constituent assembly to acquire greater powers, voted in by proportional representation.

- Zero homelessness and full reimbursement for prescribed health care.

- Recognize burn-out as an occupational disease.

- Sharp-tongued Mélenchon galvanizes left.

- Abandon nuclear power

- Renegotiate the terms of France’s EU membership

4- What does Fillon want:

- To scrap half a million public sector jobs and the 35-hour work week

- Removing the wealth tax (ISF)

- To strip jihadists returning from the wars in Iraq or Syria of French nationality

- Requiring parents in receipt of social allowances to agree to a "parental responsibility contract", to tackle children's absenteeism or behaviour "disrespectful of the values of the [French] republic"

- Lifting EU sanctions on Russia and helping Syrian President Bashar al-Assad defeat so-called Islamic State (IS).

Who will win?

According to pollsters, 48-year-old Le Pen, an anti-EU candidate, is expected to qualify for the second round but ultimately lose to Emmanuel Macron, 39. A Le Pen victory would send shock waves every bit as seismic as events in the UK and US, likely spelling the end of the European Union in its current form. Her victory would also domestically test the country's already strained relations with its sizable Muslim community.

What will happen to EURO?

Now we have established the above candidates and their agendas, the main concern for traders and EURO future levels are whether France will stay in EU or depart. Le Pen and Macron are more likely to qualify for the second round, but that's not the problem. Le Pen ( Anti EU ) and Macron ( Pro EU ) will still commit to EURO bear and bull forces.

Scenario 1:

If Macron was on top and Le Pen second, optimism will arouse as France will still be part of EU cartel despite Le Pen qualifying for second round taking into consideration that Macron scored more votes which should boost and energize EURO facing U.S Dollar rival.

Scenario 2:

On the other hand, if Le Pen came first and Macron second, this indicates that Le Pen odds of heading the final round will more likely increase and the doubt about Frexit will start creeping into minds, which will result in EURO collapsing.

Scenario 3:

A qualification for Mélenchon will still support French EU membership although Mélenchon calls for a reformation between France and EU treaties, but has never called for a break from EU union.

Scenario 4:

Fillon (Pro EU) support France being part of the EU and calls lifting sanctions on Russia which should ease the tension between Europe and Russia, and this could result in economic growth for both countries as they both benefit and EURO could boost up on positive expectations.

Technical overview:

" Note: This analysis is intended to provide general information and does not constitute the provision of INVESTMENT ADVICE. Investors should, before acting on this information, consider the appropriateness of this information having regard to their personal objectives, financial situation or needs. We recommend investors obtain investment advice specific to their situation before making any financial investment decision. "

Oil Bullish Forces In Action Over OPEC Deal Extension, Eyes on U.S Inventories

.webp)

The long waited deal between OPEC and Non-OPEC counties has finally saw the light as we mentioned in the last article we posted. Yesterday, oil levels surged +$0.94, with a high 48.73, highest levels for this week and today, crude extended bullish candles with 48.57 with expectations to surpass Wednesday's highs. Crude levels were confined with $1.65 price action with six consolidation consecutive sessions indicating low volatility as markets were anticipating hints from either U.S increased shale drilling or from OPEC striking a newer deal, other than Vienna.

API data showed U.S. crude supplies up 1.9 million barrels. The American Petroleum Institute late Tuesday reported a rise of 1.9 million barrels in U.S. crude supplies for the week ended March 24, according to sources. The API data also showed a decline of 1.1 million barrels in gasoline supplies and a fall of 2.0 million barrels in distillates, sources said. Supply data from the Energy Information Administration will be released Wednesday morning. Analysts polled by S&P Global Platts forecast an increase of 300,000 barrels in crude inventories.

Between the U.S and OPEC, another fundamental catalyst logged the field, (Libya) an armed protesters blocked Sharara and Wafa oil western fields, reducing output by 252,000 barrels per day (bpd), a source at the National Oil Corporation (NOC) told Reuters late on Tuesday.

MOSCOW (Reuters) - Russia and Iran have pledged to continue efforts to rein in oil production and stabilize markets, the presidents of both countries said in a joint statement on Tuesday. "Russia and Iran will continue cooperation in this sphere (in oil output cuts) in order to stabilize the global energy market and ensure stable economic growth," the statement from Russian President Vladimir Putin and Iranian counterpart Hassan Rouhani said.

According to Bank of America Merrill Lynch, U.S. oil production growth between September and December was almost entirely the result of offshore wells, which increased production by 220,000 barrels a day in that period. Offshore projects are much more long-term investments. They are far more costly to develop and take years to get started. "Those projects have an inertia," said John Kilduff of Again Capital. Total U.S. oil production peaked at 9.6 million barrels a day in 2015 and fell to 8.56 million by September, according to Energy Information Administration data. Since then, U.S. production has jumped back, reaching 9.1 million barrels a day this month, according to the latest EIA weekly data. (CNBC).

The Organization of the Petroleum Exporting Countries (OPEC), along with some other producers including Russia, have agreed to cut production by almost 1.8 million bpd during the first half of the year in order to rein in a global fuel supply overhang and prop up prices. But as markets remain bloated halfway into the cuts, there is a broad expectation that the supply cuts will be extended into the second half of the year. Despite the rising consensus of extended cuts, the OPEC-led strategy to re-balance oil markets is not without controversy. As OPEC and especially Saudi Arabia cut their production, other producers not participating in the cuts have been quick to fill the supply gap and gain market share. (Reuters).

In the United States in particular, shale oil drillers have seized the opportunity to ramp up output and exports. As a result, China became the third biggest overseas destination for U.S. crude oil in 2016, according to data from the Energy Information Administration (EIA), up from ninth position the previous year.

"In 2016, U.S. crude oil exports averaged 520,000 bpd, 12 percent above the 2015 level, despite a year-over-year decline in domestic crude oil production," the EIA said.

Conclusion: Currently, the U.S has the upper hand controlling oil bearish levels, but given the above fundamentals between Libyan oil field issues and OPEC and Non-OPEC deal waving on horizon, crude levels could steady back to $50>$52 pb, that's if and only if. Otherwise, crude levels will sustain the $47>$49 pb.

Remark : Look forward for U.S Crude inventories set to be released today at 3:30 PM GMT and forecasts are 1.2M compared to 5.2M on previous sessions. The above fundamentals are the key player and markets should pay attention about what's coming next, either from OPEC or perhaps another new fundamental other than Libyan protesters, which could tackle oil prices upward or downward.

GBP/USD Digests Monday's Gains Ahead of Article 50 Release

Sterling lost the sharp tone yesterday and went to a softer one today as UK gears up for the historic release for Article 50. GBP/USD bled -239-pips since Monday and plunged to 1.2376 low today over fears of consequences of what might outcome as PM releases the article. Traders has abandoned buying positions of GBP/USD high levels and left the pair to cast at lower levels with aggressive selling. On the other hand, U.S Index is showing a minor recovery today, with +$0.71 increase following positive U.S Consumer Confidence release yesterday with a positive 125.5 compared to 116.1 on previous sessions.

PM May has already signed the Article 50 letter, which will be delivered by Tim Barrow today at 11:30 GMT. Thereafter, the European Council (EC) President Donald Tusk will hold a press conference at 13:45 GMT on the UK Article 50 notification. The UK PM May finally invoking the Article 50 means the process of the Britain to exit EU’s membership commences, after the referendum vote held in June last year showed Brits favoring a Brexit by 51.9% to 48.1%.

Once the Article 50 is triggered later today, the terms of Britain's exit will have to be agreed by 27 national parliaments, a process which could take some years. Some EU leaders believe, it could take as long as 5 years to agree to new trading and immigration policies with the remaining countries In the meantime, the UK will continue to abide by EU treaties and laws.”

Timeline post-Article 50 trigger (via the Sun)

MARCH 31: Donald Tusk will give the EU’s remaining 27 member states’ initial response to Mrs May.

APRIL 29: Emergency summit of the 27 EU leaders to agree on the mandate for their lead negotiator Michel Barnier to conduct exit talks.

MAY 7: French presidential elections final run-off. Many believe serious talks cannot begin until we know who the next French president is.

MID MAY: Michel Barnier draws up EU’s negotiating guidelines based on the mandate given to him. The EU’s council of foreign ministers meets to sign them off.

LATE MAY/EARLY JUNE: Face-to-face Brexit negotiations between Britain and the EU begin.

SEPT 24: German elections, to decide if Angela Merkel continues as Chancellor or is ousted. Difficult for much to be agreed on Brexit until then.

OCTOBER 2018: Both sides want to conclude negotiations six months before Britain leaves the EU to give the Houses of Commons and Lords, as well as the European Parliament and other national assemblies, time to ratify the final Brexit deal.

We could see a ‘soft’ Brexit landing if the UK agrees to compromise on issues like the free movement of people in order to maintain access to the EU single market. Contrarily, a ‘hard’ Brexit would be inevitable, in case the UK fails to reach a deal for the single market access with the EU.

Remark: Due to uncertainties evolving currently around UK with correlation of Article 50, and U.S Index sudden recovery, market to expect high volatility for GBP/USD. A break above 1.2464 projects additional bullish waves towards Monday's range at 1.2535 & 1.2605. The opposite scenario, A penetration for 1.2337 will increase further selloffs and wash towards 1.2241 & 1.2112 intensively. UK economic data today could be ignored due to Article 50 topic being the main frame for Sterling.

Wallowing U.S Index and Supper Yellen with Possible Scenarios

Since FOMC epic decision with 0.25% hike to initial 0.75%, U.S Index has collapsed dramatically. After peeking to $102.26 Feb-highs, the Index has shed -$2.94 and anchored yesterday at $99.32, closing to 2017 lowest at $99.19. Below are the factors contributing to bearish U.S Index Foreces.

1- Markers had already priced in and traded on the fact that Fed hike was inevitable. So basically, the FOMC decision had zero contribution to the market "Buy the rumor sell the fact " fitted like the last peace of puzzle and the USD decline picture was drawn.

2- Traders were awaiting further instructions by Yellen and Co. about coming Fed hikes, but details were not listed.

3- Doubts about Trump's capacity to provide the right leadership for Republican party have been creeping into the market fueled by allegations about links of his election campaign with relation to Russian contributes and recent Trump's real estate bought by Russians as Greg Gibbs, Director at Amplifying Global FX Capital pointed yesterday. Also Trump's bombastic style including wild claims about wire taps for the white house when he addressed journalists in previous appearances.

Fact : Combine these above elements, no wonder why U.S Index has tumbled and in case of further declines, it's logic.

Now after we have briefed the above, the real question is, How will Yellen play along today when she appears preceded by U.S Unemployment Claims. If Yellen came out with promises about coming hikes, markets will start pricing in and trading on her words and the whole cycle ( U.S Index ) will be repeated again as Déjà vu. Recent speeches of FOMC's members Dudley and Evans with their declrelations supports the coming scenario further more. So, Yellen will try to avoid this scenario and turn into different aspect in which she will focus on how strong the U.S economy is supported by positive unemployment data, inflation rate, recent CPI, NFP, and retails sales which should boost U.S Index to a 100.46 where trend will make a reverse and turn bullish.

Remark: Previous unemployment claims were 240K and forecasts for today are 241, narrowing down the gaps between the number, skepticism or confusion about comparison between recent, initial, and forecasts will be tight. Traders always tend to read the data in different way when recent is more than forecasts but less then previous, along with it, bearish and bullish volatility.

Oil levels Declines Over Concerns Of Bloated U.S Storage, Awaiting U.S Inventories

Fundamentals :

Oil prices dipped on Wednesday at 47.80 low as rising crude stocks in the United States underscored an ongoing global fuel supply overhang despite an OPEC-led effort to cut output. U.S. crude oil inventories surged by 4.5 million barrels in the week to March 17 to 533.6 million barrels, the American Petroleum Institute (API) said late on Tuesday.

"The American Petroleum Institutes' crude inventories stuck the knife into crude overnight, coming in at a 4.5 million barrel increase against an expected increase of 2.8 million barrels," said Jeffrey Halley, senior market analyst at futures brokerage OANDA in Singapore.

"If the API stuck the knife in, tonight's EIA Crude Inventory figures may twist it. A blowout above the 2.1 million barrel increase expected, may well torpedo oil below the waterline," he added.

New production projects and a fresh shale boom could boost oil output by a million barrels per year and result in an oversupply in the next couple of years, according to Goldman Sachs.

OPEC's landmark decision to limit output for the first time in eight years in a bid to arrest the existing supply glut reduced price volatility and increased stability, unintentionally helping the shale producers, the bank said.

"OPEC's decision in November 2016 to cut production was rational, in our view, and fit into its role of inventory manager of last resort," Goldman said.

"However, the unintended consequence was to underwrite shale activity through a bullish credit market at a time when delayed delivery of the 2011-13 capex boom could lead to record non-OPEC production growth in 2018."

The Organization of the Petroleum Exporting Countries (OPEC) agreed to curb its output by about 1.2 million barrels per day (bpd) from Jan. 1 this year. Russia and 10 other non-OPEC producers agreed to jointly cut by an additional 600,000 bpd.

Sources within the Organization of the Petroleum Exporting Countries have indicated that its members increasingly favor extended production cuts but want the backing of non-OPEC oil producers, such as Russia, which have yet to deliver fully on existing reductions. ( CNBC )

PEC compliance in Feb 2017 was estimated over 94% which helped oil boosters to sustain levels above $52 bp on average but the war continues between the US and OPEC counties with opposed interests.

Russia has reduced oil production through first 2017 quarter by 200000 bpd and promised to increase further reductions to 300000 bdp by end of April or May with OPEC plan being in accord. According to sources to CNBC, OPEC is on the edge of striking a powerful strike where the cartel is considering extending initial Vienna deal till end of 2017 if OPEC and Non-OPEC counties agree to further oil reduction to curb market demand, but details about quotas were not specified. Markets, although OPEC next move is currently cooked in a low steam, are looking forward for such deal in which, in case established or achieved, should energize oil bullish levels back to Feb 2017 prices.

Conclusion : Currently US has the upper with increase shale drilling and inventories storage. The rift continues and the war tone is ascending between U.S and OPEC, each trying to drive oil levels higher and lower depending on their economic interests. Keep an eye on OPEC next chess move which will set oil course for the coming weeks. Look forward for U.S crude inventories today set for a release at 2:30 PM GMT.

Technical Overview

The market currently bearish due to the above mentioned data, but OPEC keep an eye on OPEC coming moves. If OPEC managed to struck the deal with extension till end of 2017, crude levels will sustain the $50>$52 levels. In absence of news from Organization of the Petroleum Exporting Countries, markets should expect further declines with $47<$46 as targets.Crude Oil Plunged Over Concerns of An Increase On U.S Shale Drilling

.webp)

U.S has finally nailed the bulls eye and managed to plunge oil levels below $50 pb at 47.08 2017-fresh-lows. Today, oil prices managed to make an correction with a gain of $1.71 with 48.79 high, and currently oil is pushing for additional profits, lifted by lifted by a surprise draw-down in U.S. inventories and helped by figures from the International Energy Agency (IEA) suggesting OPEC cuts should push the crude market into deficit in time.

"For those looking for a re-balancing of the oil market the message is that they should be patient, and hold their nerve," the IEA said in its monthly report.

The IEA reported global inventories rising in January for the first time in six months despite OPEC cuts since Jan. 1, but said if OPEC stuck to limits the market should see a deficit of 500,000 barrels per day (bpd) in the first half of 2017.

OPEC's compliance with output cuts remained high even though the group's monthly report indicated a rise in global crude stocks and a production jump from Saudi Arabia, Goldman Sachs said on Tuesday. Goldman said in a research note that market re balancing is still progressing, and it saw demand for oil finally exceeding supply in the second quarter aided by production cuts, despite an expected rise in U.S. shale output.

However, OPEC on Tuesday reported a rise in oil inventories and raised its forecast for production in 2017 from outside the group. It said its biggest producer, Saudi Arabia, increased output in February by 263,000 barrels per day (bpd) to 10 million bpd.

The Organization of the Petroleum Exporting Countries is curbing its output by about 1.2 million barrels per day (bpd) from Jan. 1, the first reduction in eight years. Russia and 10 other non-OPEC producers agreed to cut half as much.

OPEC said in the report oil stocks in industrialized nations rose in January to stand 278 million barrels above the five-year average, of which the surplus in crude was 209 million barrels and the rest refined products.

"Despite the supply adjustment, stocks have continued to rise, not just in the U.S., but also in Europe," OPEC said.

"Nevertheless, prices have undoubtedly been provided a floor by the production accords."

In the report, OPEC pointed to an increase in its members' compliance with the deal, according to figures from secondary sources that OPEC uses to monitor output.

Supply from the 11 OPEC members with production targets under the accord - all except Libya and Nigeria - fell to 29.681 million bpd last month, according to these figures.

That means OPEC has complied by more than 100 percent with its plan to lower output for those nations to 29.804 million bpd, according to a Reuters calculation. OPEC gave no compliance figure in the report.

But the report revised up its estimate of oil supply from producers outside OPEC this year, as higher oil prices following the supply cut help spur a revival in U.S. shale drilling. ( Reuters )

Production outside OPEC is now expected to rise by 400,000 bpd, 160,000 more than previously thought. U.S. oil output in 2017 was revised up by 100,000 bpd.

Finally with the significant down-drawn in U.S shale and forecasts for U.S inventories today is 3.3M compared with previous week 8.2M, we are looking for an ascending increase for oil price.

Remark : Look forward of U.S Curde Inventories today at 2:30 PM GMT.